Inflation is rising: Here are 5 ways it could impact you

Prices of everyday goods are rising at a pace not seen in a decade, and investors are paying close attention. Here are some ways it could impact your finances.

Have you tried to buy a car lately, but didn’t remember the price being so high? Or maybe you’re renovating a house, but your contractor keeps telling you how expensive lumber is these days? It’s not a coincidence. Over the last few months prices on many consumer goods, from food to housing to gasoline, have climbed.

In May, Canada’s Consumer Price Index (CPI) — the metric which measures the change in price of a set basket of consumer goods and services — jumped by 3.6% from a year earlier, the highest increase in a decade. Other items not included in the CPI, like commodities such as copper and lumber, have also spiked, with the latter rising 261% on the Nasdaq between January 2020 and May 2021.1

These price gains are what’s called inflation, a term many Canadians have likely seen in news headlines. It’s worth paying attention to as rising prices could impact your finances, though inflation may not be as scary as you might think.

How does inflation work?

Inflation follows the basic law of supply and demand. Higher inflation suggests that demand for goods and services is rising faster than the economy’s capacity to produce them. Take lumber: With so many homeowners stuck inside over the last year, demand for two-by-fours and other wood products needed to renovate or build new homes has soared, while supply couldn’t keep apace. The result? Higher lumber prices.

For the most part, rising prices shouldn’t raise much concern. Inflation can be a sign of a strong economy, and central banks in both the U.S. and Canada generally expect to see prices rise by between 1% and 3% per year. We’re talking about this now, because as the economy enters what many expect could be a post-pandemic boom, there is some concern that prices could jump too high too quickly. If everyone starts spending again, and jobs come back, then demand for all kinds of goods and services could increase, which would push prices higher.

So what does inflation mean for your money? Here are some ways everyday Canadians can feel the effects of inflation:

Higher cost of living

One main effect of inflation is a potentially higher cost of living. The more prices rise, the more money you’ll need to spend on buying items. While you can cut back on certain things, such as travel or home furnishings, you’ll still have to buy others, like food or gas for your car. If you have a budget, accounting for inflation is simple: Increase your spending in the areas most important to you, while cutting back in others.

Purchasing power erodes

You can’t have a conversation about inflation without mentioning purchasing power, which refers to how much one unit of money can buy. Rising prices will have an impact on your purchasing power, especially if your income stays stagnant. How? One dollar might buy you something today, but if that item costs $2 tomorrow, and you haven’t earned more money to keep up with the price gain, then your ability to buy that item has decreased.

Need for more income

If your purchasing power is being eroded, then you’ll need to somehow earn more money. Many jobs offer annual wage increases in line with inflation, which means if inflation rises by 2% then your salary should rise by as much. In that case, you may not notice that costs have climbed. If prices increase too rapidly, though, then you may have to ask for a higher pay raise, and your boss may or may not oblige.

Potentially reduced savings rates

Inflation can also make it more difficult to save. If you’re keeping money in, say, a high-interest savings account that pays 2% interest per year, while inflation rises by 1%, then you’ve made what’s called a 1% real return. However, if inflation rises by 3%, then you’ve essentially lost money in that account because prices have climbed by more than what you’ve earned. On the flipside, interest rates usually rise with inflation, which means savings account rates could become more attractive.

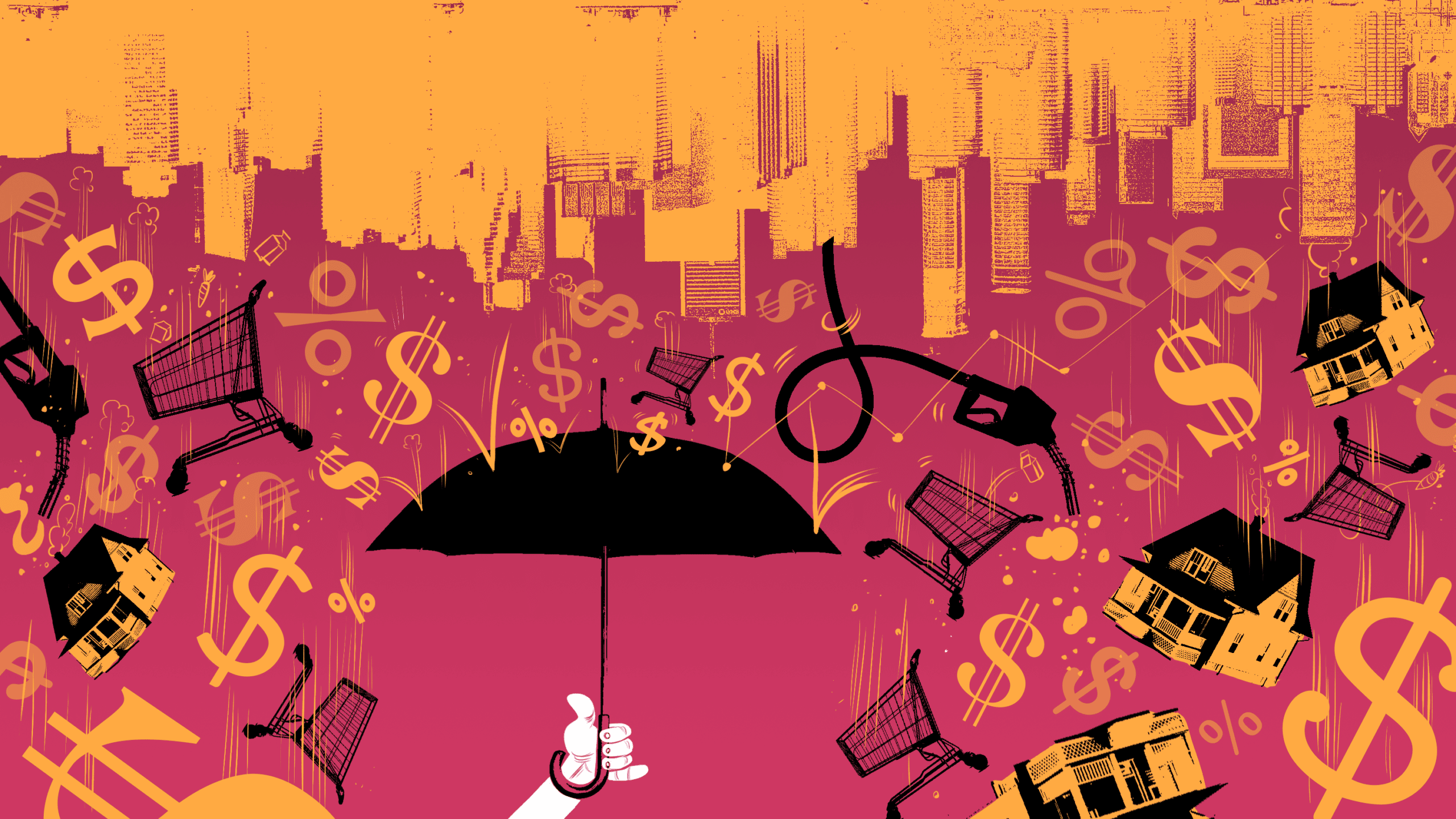

Your investments need to keep up

Many investors maintain a diversified portfolio, but not all investments react the same way to rising prices. Historically, gold and real estate prices have tended to climb along with inflation, while bonds and dividend paying stocks have declined in value. When and how fast inflation happens can have an impact on your investments and, while you may not understand all the mechanics of the market — the professionals who think about this every day can handle that — you might consider ensuring you own a variety of diverse assets, including some that can benefit from inflation. This way, your portfolio has the opportunity to not only keep up, but to also grow.

At the moment, economists aren’t worried this heated inflation is going to last. One reason why inflation climbed by so much in May was because the costs of many goods dropped a year earlier thanks to the pandemic’s first lockdown. Supply chain issues throughout the COVID-19 pandemic have also put pressure on supply and demand for certain goods, but TD Economics has said those issues could ease in the coming months. It adds that inflation will remain a bit above 2%, which is in the range that central banks want to see.2

As with many aspects of your finances, it can be important to pay attention, but you may be wary of making sudden moves. If you have a solid budget, good long-term goals and a diversified portfolio, you may not even notice that some of the things you buy are now more expensive.

BRYAN BORZYKOWSKI

MONEYTALK LIFE

ILLUSTRATION

VERONICA PARK