How might your personality affect your investments?

Find out how your investing personality may be driving some of your best and worst investing decisions.

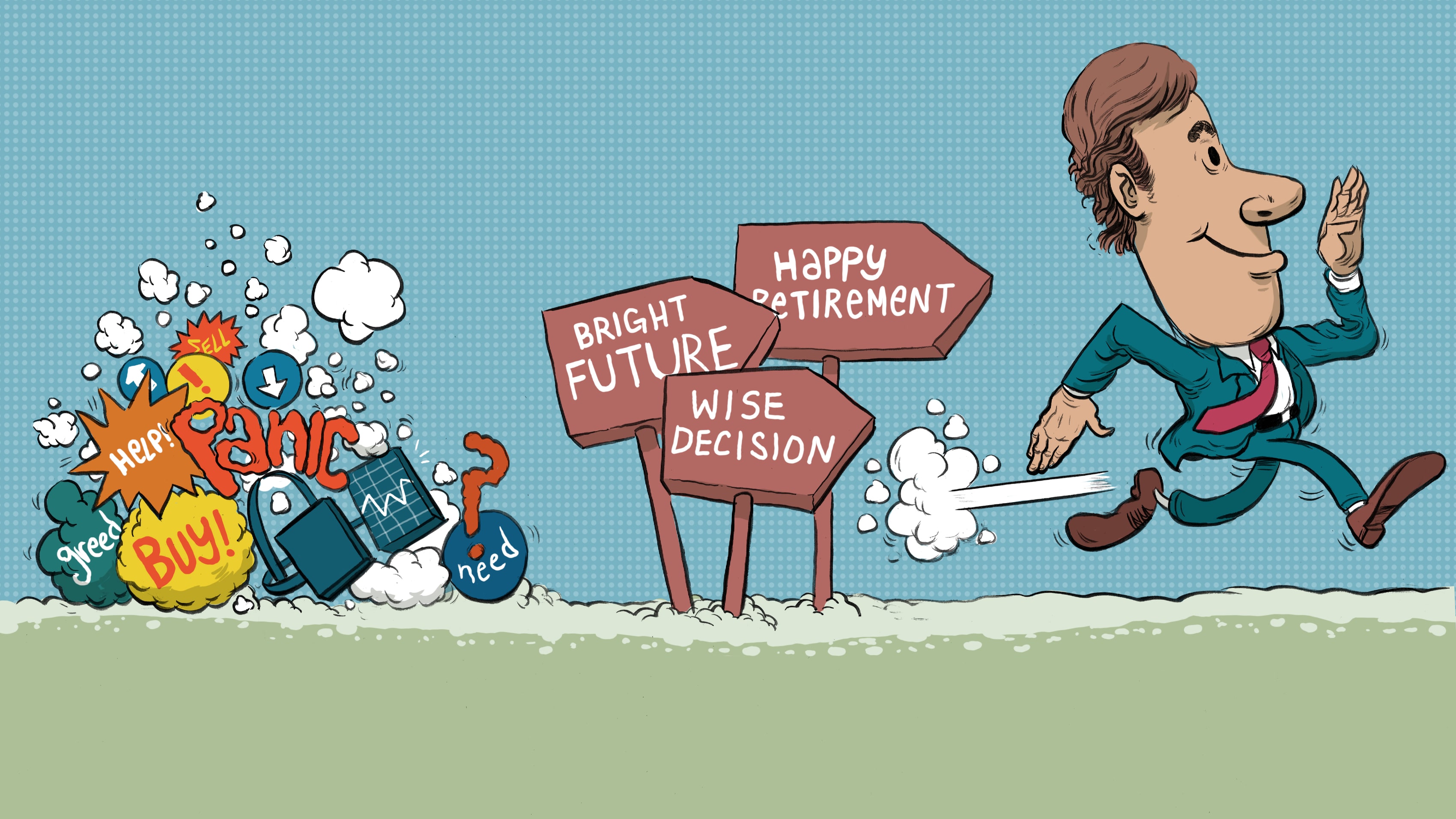

Succeeding at investing may be just as much about dealing with forces beyond your control as it is about managing the elements you can control.

And while it may be painful to admit, one of those uncontrollable factors is yourself. Decades of scientific research has discovered that our personalities can influence how we make financial decisions. Moreover, studies indicate that learning about our attitudes and biases can help us make better money decisions.

For example, the recently published TD Wealth Behavioural Finance Industry Report, 2021: A Behavioural Perspective on Risk, found that those who had a volatile income or worked in a volatile industry were 2.5 times more likely to select a more volatile portfolio, whether they realized it or not. But what came next may also be telling: They were also four times less likely to be satisfied with their readiness for retirement.

“Working with an advisor who knows your personality can bring about better choices, especially when the markets are rocky or when you’re going through a financially stressful time like a divorce or buying a house,” says Lisa Brenneman, Head of Behavioural Finance, TD Wealth.

Here are five personality traits that can influence how we look at investing, risk management and financial decision-making. Knowing more about yourself and where your personality aligns with these traits can help you deploy tactics — such as relying on professional advice — that can aid in making better decisions around money.

Extraversion

A party can be an excellent place to view extremes of this quality: Those with outgoing natures and the tendency to seek attention are easy to spot, while the more reflective and reserved among us may spend the evening quietly in the corner. Higher extraversion can also result in riskier behaviour, such as overpaying for financial assets. Advisors can help by providing a clear focus and direction for a financial plan — both in the short term and the long — and by revisiting it often.

Agreeableness

People who score highly for this trait may be more trusting and cooperative versus those who may be more inquisitive and have a challenging personality. Those with low agreeableness may be likely to take greater risks. Understanding the balance between risk and reward is essential when investing, and it’s important to appreciate your risk tolerance and capacity. Determining your financial goals and talking about risk is one way working with a planner can help.

Conscientiousness

If you can ignore that tempting bag of cookies until the weekend, you might score high on conscientiousness. This feature can be characterized as an ability to deny immediate gratification in exchange for fulfilling future goals: In other words, being self-disciplined and organized vs. living in the moment.

In personal finance, those who score low on this attribute may have challenges saving for a long-term goal like retirement. An advisor may help by suggesting strategies like preauthorized automatic transfers which can grow savings with little regular effort.

Reactiveness

A person with this quality in abundance may be highly responsive to emotional stress, as opposed to someone who is calm and relaxed. Unfortunately, the investing world is full of headlines that may trigger someone emotionally, and a highly reactive person may do damage to their portfolio or finances by making poor knee-jerk decisions. An advisor can help an investor both put market events into the proper context and avoid over-reactions to unwelcome news.

Openness

This characteristic can describe someone who is curious and creative at one extreme or conservative and cautious at the other. The problem with these last two traits is that investing always requires a certain amount of risk: Being timid could mean keeping funds in cash which would make it harder to meet goals like retirement. An advisor can help someone like this by creating an investing plan that satisfies the need to grow assets while also managing the proper risk profile for the individual.

“Whether you are aware of them or not, all these traits have an impact on your investing style. Fortunately, learning to be a better investor now can avoid years of imperfect investment choices,” Brenneman says. “When your advisor is equipped to understand you better, they can help you avoid mistakes.”

DON SUTTON

MONEYTALK LIFE

ILLUSTRATION

VERONICA PARK