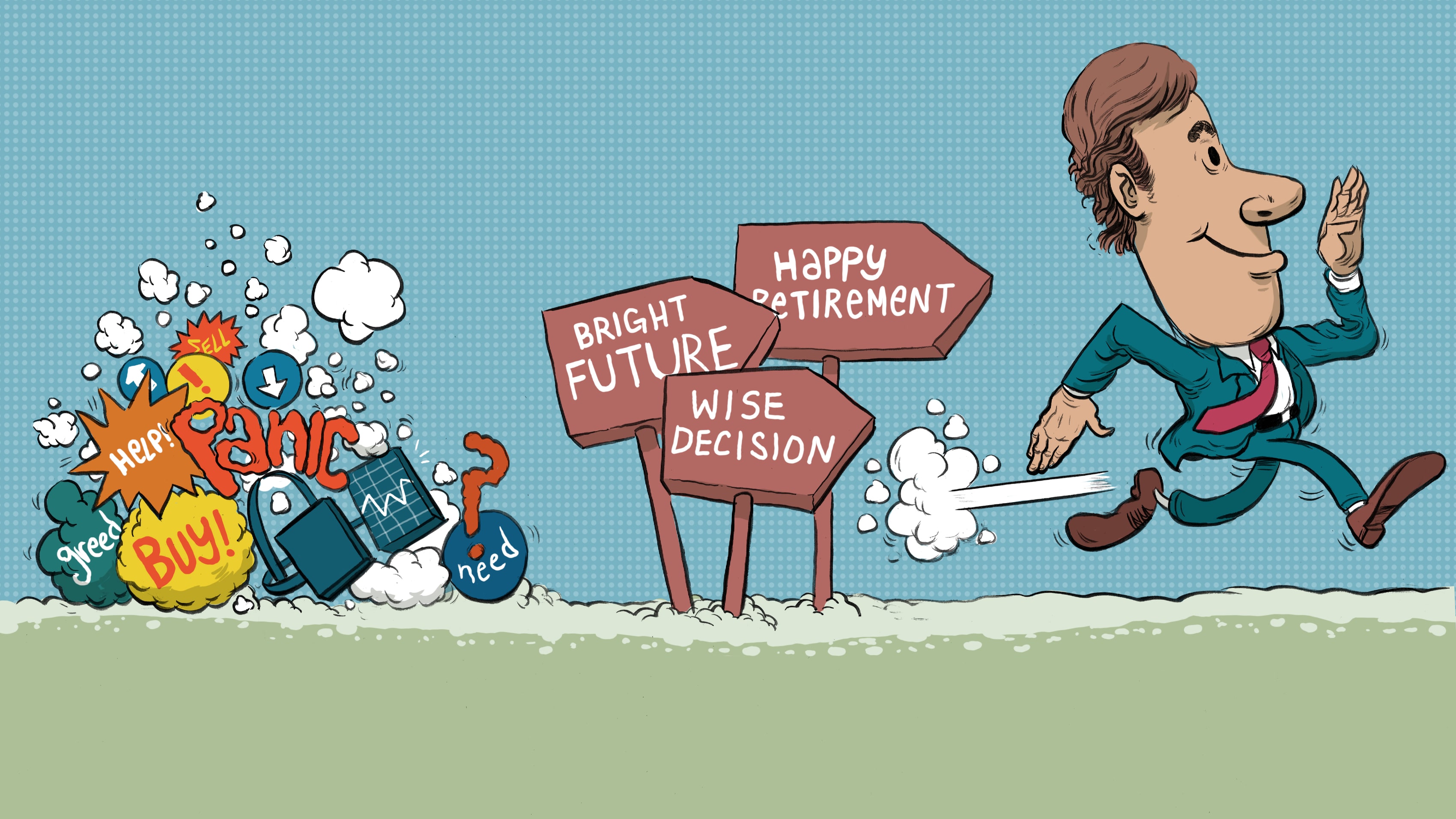

Can this personality trait help you thrive in a recession?

For most of 2022, the markets were mucky. But in the face of any downturn, your day-to-day perspective could have an impact on whether you thrive or merely survive.

ANTHONY DAMTSIS

DEPUTY HEAD OF BEHAVIOURAL FINANCE, TD WEALTH

The prospect of a looming Canadian recession dominated the news cycle through the autumn months of 2022. Who could be most affected? How long could it last? In most cases, economists can look to the data to build their perspectives, with no need to bring emotions into the equation. However, the answer to the most important question won’t be found in an economic forecast.

What many people really want to know is, “Am I going to be OK?”

Trying to answer that question by sorting through the available data can lead us down a path of paralysis by analysis. It hardly seems to be the right way to approach such an emotion-driven question. Another way to answer this question would be to lean into our emotions to uncover what motivates us during periods of economic uncertainty.

As a trained behavioural economist, I can tell you that our personality plays a much larger role in how we make money decisions than many traditional economists might care to admit. For example, research has shown that our ability to remain confident that we are on the right financial path and can weather economic storms is strongly related to one specific personality trait — reactiveness.1 Understanding how and why this trait affects our judgement is an important first step in mastering our mind so our money doesn’t master us.

Reactiveness is one of the “Big Five” personality traits that psychologists study, along with extraversion, agreeableness, conscientiousness and openness. Each trait exists on a spectrum, and each end of the spectrum offers its own benefits and pitfalls when it comes to financial decision-making.

When it comes to reactiveness, those who are quick to react are more likely to experience stress during periods of market volatility, whereas those who tend to remain calm under pressure are often more resilient and optimistic, to the point of experiencing something known as optimism bias.

Optimism bias is a behavioural phenomenon where people tend to think positive outcomes are more likely to happen than they really are (and underestimate the likelihood of negative outcomes). It is highly correlated to being calm under pressure.

The cause of optimism bias can vary, but for many people, it may be rooted in a need for control. Dwelling on negative outcomes, such as losing value in one’s portfolio, can threaten our future and quickly become overwhelming, so instead, we minimize the perceived likelihood of a negative event occurring. This can lead our minds into some curious contradictions.

For example, during the 2020 economic downturn, researchers found that though many people had a pessimistic view of their country’s economic future, they had a positive outlook about their own economic situation.2 As participants in their country’s economic future, it is more likely that their own financial situations would follow their country’s — and decline! This disconnect between expectations and reality is clear evidence of optimism bias.

Embracing the benefits of being optimistic

Is having optimism bias a bad thing? Perhaps not. Behavioural biases are often portrayed as unwanted and there are plenty of articles that highlight how biases can lead many of us to make bad decisions that lead to bad outcomes — and they are mostly right. However, there are times when a behavioural bias can be beneficial.

For equity investors, for example, there’s evidence that optimism bias is correlated to higher returns.3 This may be because optimistic investors tend to stay invested in the market, while those who are more pessimistic may resort to the “safety” of cash, despite the corrosive effects of inflation.

Another perk of being calm under pressure during recessions? The optimistic among us tend to be more resilient. In other words, they can bounce back from stressful situations more easily than quick-to-react individuals. When portfolio values decline significantly, resilient investors may be better able to adapt to changing market conditions, for example, by making small adjustments to their portfolio’s asset allocation or identifying opportunities to harvest tax losses.

But what if I’m less optimistic?

Being calm under pressure has its perks, but don’t despair if you identify as quick to react. There are several things you can do to recalibrate and make cool-headed money decisions.

The first thing you might consider doing is speaking with your financial advisor. Not only is reaching out for help a great way to build resilience, your advisor also has a depth of knowledge on investing and other money matters. They can help you see that you’re not alone in your worries. They may also be able to help you shift your perspective to the long term, and realize that short-term fluctuations in your portfolio’s value may not prevent you from reaching your goals.

You might also consider taking a break from constantly checking your portfolio, especially if you’re one of the many people who look every day. Others have done the math: If you’re checking your portfolio daily, there’s nearly a 50% chance, based on past performance, that it will show a loss from the day before.4 Those who prefer more good news should try checking annually. Historically speaking, the S&P 500 has generated a positive annual return seven years out of every 10.

Recessions and recoveries tend to go hand-in-hand. If you have the right temperament and tools at your disposal, a downturn may actually be an opportunity to thrive, not just survive.

If you’re unsure of whether you are more quick to react or calm under pressure, book an appointment with a TD Wealth professional. They may be able to help uncover your financial blind spots and tailor their advice to your needs so you can master your money decisions.

Anthony Damtsis is currently Deputy Head of Behavioural Finance at TD Wealth. He has worked in the field of behavioural finance in the U.S. and Canada and holds graduate degrees in both economics and behavioural science.

- TD Wealth Behavioural Finance Report 2021, “A behavioural perspective on risk,” www.td.com/content/dam/wealth/document/pdf/wealth/industry-report-a-behavioural-perspective-on-risk-en.pdf Accessed on November 24, 2022 ↩

- Barrafrem, K., et al. Financial well-being, COVID-19, and the financial better-than-average-effect. 2020. Journal of Behavioural and Experimental Finance. ↩

- R. Renu Isidore and P. Christie. 2019. Model to Predict the Actual Annual Return of the Investor with the Investors’ Behavioral Biases as the Independent Variables. Journal of Private Equity. ↩

- Shlomo Benartzi, November 1, 2015. “Keep Stock Market Apps Off Your Phone” www.shlomobenartzi.com/columns/keep-stock-market-apps-off-your-phone Accessed Nov. 24, 2022 ↩