Bounce back from the retirement blues

![Bounce Back From The Retirement Blues- TD MoneyTalk Life Stories [Feat]](https://www.moneytalkgo.com/wp-content/uploads/2016/06/Bounce-Back-From-The-Retirement-Blues-TD-MoneyTalk-Life-Stories-Feat.jpg)

Many people dream of a life free of worries in their golden years. Yet some find themselves anxious and depressed when that abrupt change comes. Here are some planning tips to help make your retirement days truly golden.

May 4th, 2023

Robert Delamontagne wasn’t used to being caught off guard. After 25 years building EduNeering Inc., a software company for regulated businesses, he was adept at anticipating problems. But when he sold his company and retired his CEO post at age 63, he was shocked by the impact it had on his mental health.

“I started feeling weird emotions,” says Delamontagne. “I didn’t know if it was depression or what. I was lethargic, aimless, bored. I felt some kind of psychological pressure inside of me, like a malaise.”

With his fast-paced, pressure-filled days behind him, he says he had a hard time adjusting to his new retired life. “I went from going 1,000 miles an hour to zero miles an hour,” he says.

Be ready emotionally when retirement arrives

Retired and not being happy may sound odd to those who want to retire but Delamontagne’s experience isn’t rare. Depression is the number one mental health issue facing older Canadian adults, with retirement from work being a key trigger. 1 In fact, studies show retiring can raise your risk of clinical depression by 40%. 2

“I didn’t know if it was depression or what. I was lethargic, aimless, bored. I felt some kind of psychological pressure inside of me, like a malaise.”

Retired CEO

The fact that post-work depression is recognized as a serious issue means that everyone can consider managing the retirement blues before they happen. Mental health should be one of the many areas that is factored into someone’s retirement planning. Just like we want to accumulate sufficient funds for retirement day, we should make sure we’re also mentally ready when it arrives.

We talked to Delamontagne and some specialists about strategies for dealing with mental health in retirement.

Build a mental plan for retirement

Like in Delamontagne’s experience, depression can hit rapidly after an abrupt change in lifestyle, says Dr. Gina Di Giulio, clinical psychologist, mental health activist, CEO and Founder of Pathwell, a mental health clinic in Toronto.

“It’s more common than people think because, unfortunately, it’s not usually openly discussed. It’s especially true in the first weeks and months. There is this idea that retirement is this great thing that people look forward to. So, it can be very confusing when it arrives and yet they are not happy.”

Symptoms of depression can range from mild to severe, and can include anxiety, restlessness, agitation, sleep problems, changes in appetite or weight, decreased motivation and uncertainty about the future.

Keep active, be social

For some, being away from a work environment closes off a major source of socialization. “Being socially isolated is one of the symptoms of depression, and if people are having a hard time coping with retirement, they may withdraw more from friends and family who might be able to potentially help them adjust,” she says.

“Too much free time can trigger anxiety when structure and routine are removed, because it introduces more uncertainty into a person’s day,” Di Giulio says. “One of the scariest questions that more routine-oriented and structure-oriented people can ask themselves in retirement is, ‘what am I going to do today?’”

Becoming active by pursuing some of the things you’ve always said you wanted to do helps. “This is ideally how one should spend their time in retirement, now that the constraints of time [and] work responsibilities are removed,” Di Giulio says.

Delamontagne says he escaped his depression by, first, recognizing what was happening, and second, getting busy doing all the things he’s always wanted to do but just didn’t have the time for.

“I went on a 170 km bike ride. My family members went with me because they were afraid I was going to have a heart attack,” he says. “I went to Spain and walked the Camino Santiago, a nearly 200 km walk from France to Spain that people have been doing for 1,000 years. So, I started to do things that were out of the ordinary for me, because I felt I needed to break the mold.”

Fortunately, Delamontagne had the money to do it.

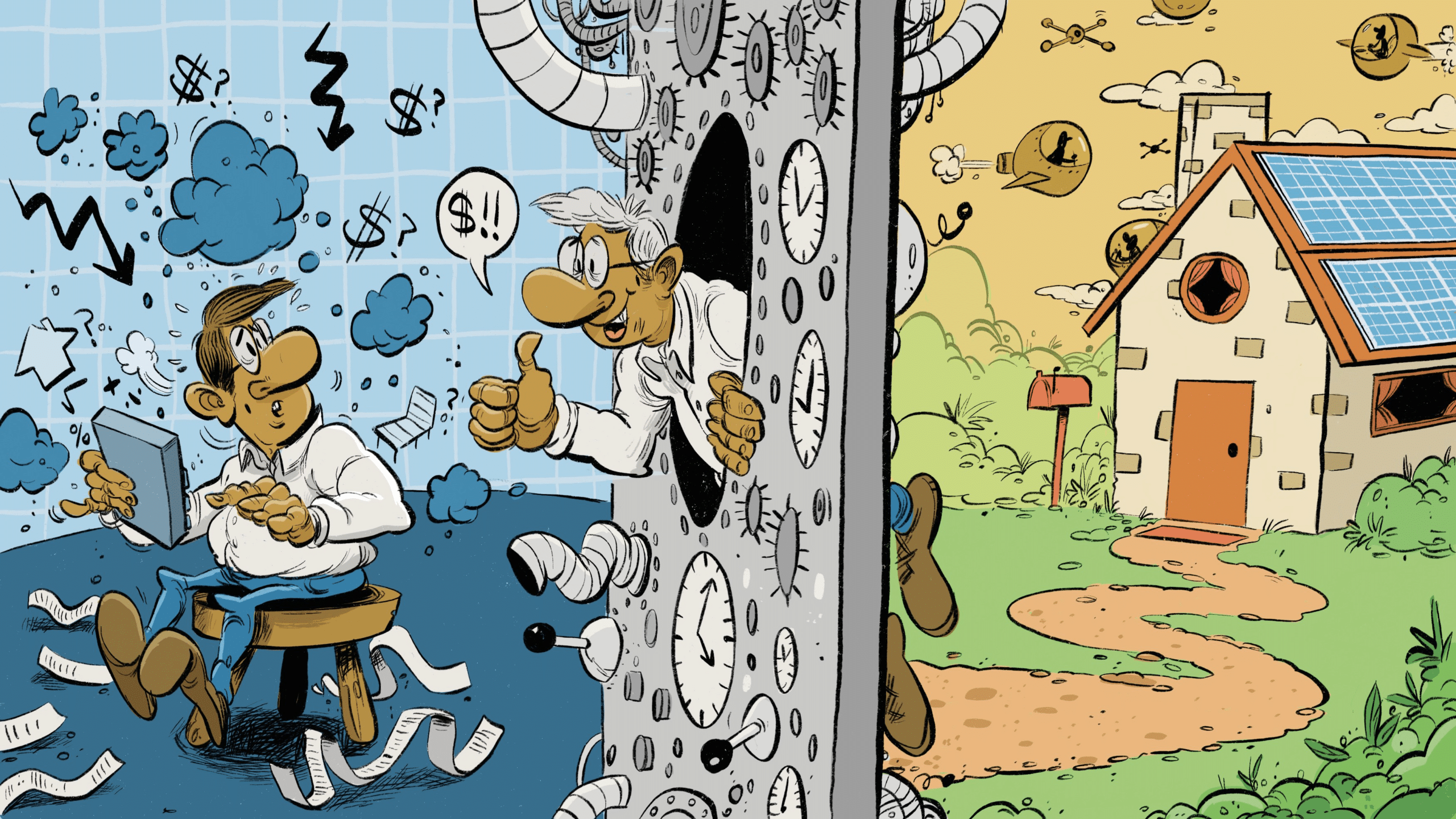

Don’t let depression disrupt retirement planning

However, for people who are depressed or anxious about retirement, the important decisions around the retirement process can cause them to avoid, withdraw from or procrastinate about retirement planning just when decisions on these issues are vital.

Equally as bad is making a snap decision about a financial problem or delegating the responsibility to someone unqualified — a friend or family member — just to push the problem away.

“One of the symptoms of depression is avoidance, behavioural avoidance, withdrawal from other people, withdrawal from tasks and responsibility. So, definitely, feeling depressed will lead to putting off larger decisions that may feel overwhelming,” Di Giulio says.

She says one of the methods to alleviate stress and anxiety is to have a mental plan: People must have a roadmap for the mental transition from a working lifestyle to a retirement lifestyle.

Planning finances ahead may contribute to a happy retirement

Reaching retirement with enough money to do what you want, when you want to do it, is the number one concern of those seeking financial advice, says Zeljka Walker, Portfolio Manager and Senior Investment Advisor, TD Wealth, in Vancouver. “It is the first question clients all ask,” she says. “It’s a conversation we have at every meeting.”

Not planning well in advance of retirement, on the other hand, can force people to work longer and take on more risk in their investments. It could also mean downsizing your property prematurely, moving to a less expensive neighbourhood or reducing your general standard of living, she says.

Walker has seen these financial compromises lead to frustration, stress, anxiety and depression in clients. “Some people have ended up in divorce,” she says, “or see their health deteriorate.”

In order to pre-empt this frustration and be prepared for when retirement day arrives, Walker stresses that pre-retirees focus on these specific aspects of planning: health, retirement lifestyle goals, the financial strategy to fund these goals and risk-tolerance.

Finally, she asks pre-retirees to envision what day-to-day living with their spouse or partner will look like. She says it’s great that couples want to spend time together but 24 hours a day in each other’s company can be a source of stress. She says compromises must be made if partners have different interests and plans in retirement. She stresses these decisions need to be discussed in the years leading up to retirement, not the morning after the retirement party.

What happened to Robert?

After a healthy dose of self-reflection and early financial planning, Delamontagne now says he is having the time of his life. Beyond travelling and setting physical challenges for himself, he’s helping others: He’s written a series of books including, The Retiring Mind: How to Make the Psychological Transition to Retirement.

The bottom line

If you are having mental health issues, talk to a doctor who can direct you to the right professional. Speaking with a financial specialist about your options before you retire is critical, Walker says. “Knowledge is empowering,” she says. “Financial plans offer scenarios to see if you can meet your goals. You have an actual plan in writing of all your assets and debts, and income and expenses. It is a clear picture of where you are now and where you are going in the future.”

DON SUTTON

MONEYTALK

ILLUSTRATION

DANESH MOHIUDDIN

- Mental Health Commission of Canada, Guidelines for Comprehensive Mental Health Services for Older Adults in Canada, For the Seniors Advisory Committee, June 2011 ↩

- “Work Longer, Live Healthier: The relationship between economic activity, health and government policy,” Gabriel H. Sahlgren, The Institute for Economic Affairs UK (IEA) Discussion Paper No. 46, May 2013. ↩