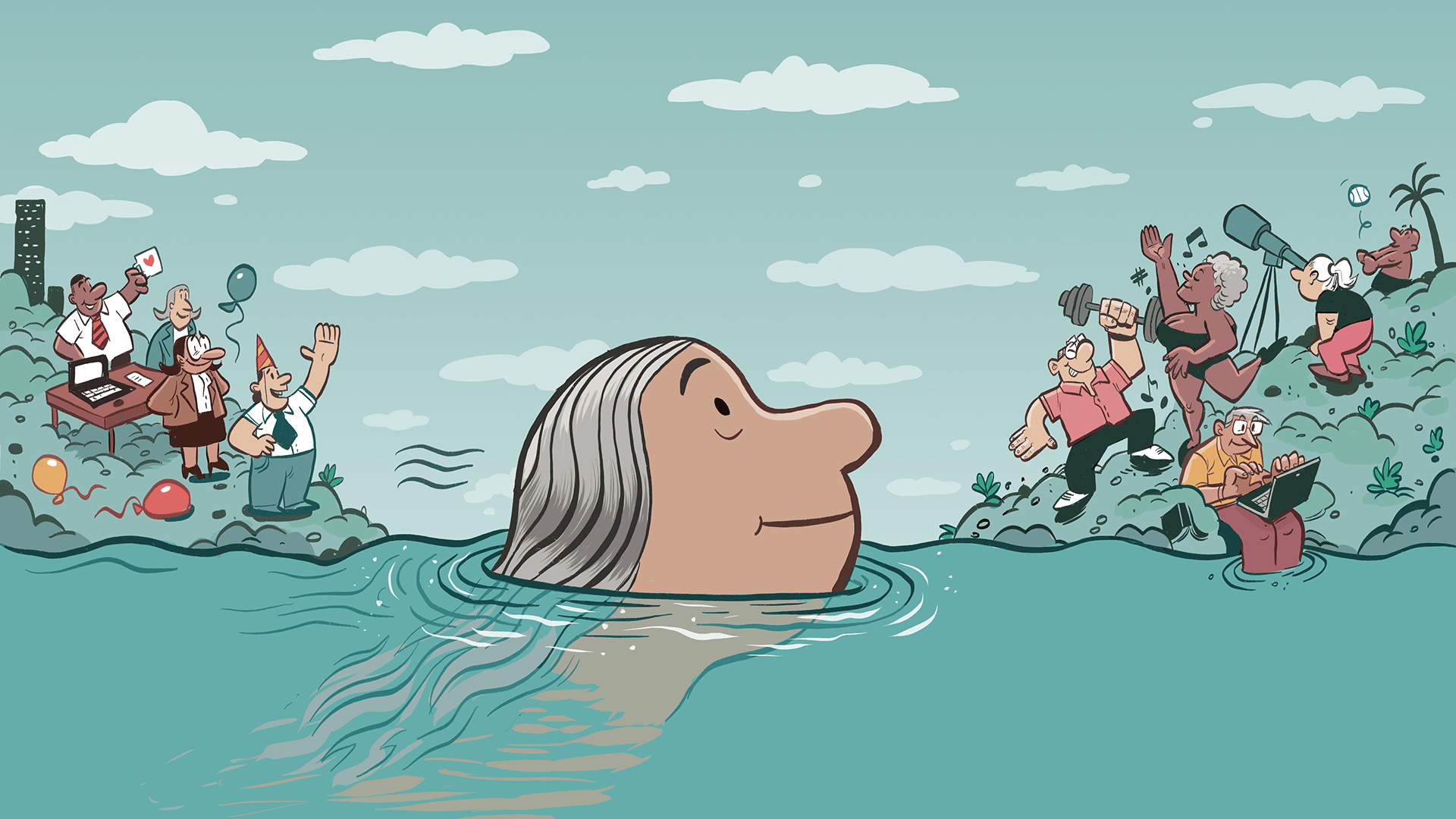

10 extra years of good health: What would you do with it?

Studies show many office workers would have little trouble working into their 70s. How could an extra decade reset your retirement plan … and maybe your whole life?

What if you didn’t retire? Is that a crazy thought?

Plenty of us would choose to retire as soon as possible if we could, and many of us may believe we will simply be too old to continue working past 70. Whether it’s by convention or experience, retiring at 65 may be the limit we focus on.

But new research suggests we may have more healthy years ahead of us than any generation before us.

A study from the Center for Retirement Research at Boston College appears to confirm a demographic trend many of us are witnessing first-hand: Older people aren’t aging like they used to. So-called seniors seem fitter and healthier than previous generations, enjoying years of good health without the debilitating conditions that have traditionally sidelined people in their 60s and even their 50s.

The study states that many people today are and will be robust enough to hold down the average office job into their 70s.1 And Canadian employment figures back that up: The number of 70-year-olds currently working full-time (171,300) is more than quadruple the number in 1988 (36,800). According to Statistics Canada, a 65-year-old could expect 16 years of good health, before age-related illnesses set in.

Knowing all of that, would it change anything about your retirement plan?

Consider this example: A senior manager with a gross annual salary of $100,000 might earn an extra $1 million if they continued working another 10 years. That’s 10 more years of your peak income, 10 more years of saving and investing, and 10 more years before you begin drawing on your retirement savings.

A sweet deal? Or a conundrum? Nicole Ewing, Director, Tax and Estate Planning, TD Wealth, says questions like these should make everyone pause and reconsider their retirement age, larger financial strategies and also their broader life plans.

“Delaying retirement could add 10 years of compound growth, presumably on a large portfolio — it’s growth on growth on growth — so your investments can increase at a much faster rate. That creates opportunities,” she says.

It’s not just those nearing retirement age who may take this information to heart. Someone in their 30s might also consider the benefits of a longer working life, Ewing says. For instance, investing in yourself at an earlier age knowing that you can work for longer may mean a bigger payoff.

What is HALE?

Statistics Canada uses an indicator known as Health-Adjusted Life Expectancy (or HALE) to measure the number of years people could enjoy before inevitable age-related illnesses set in. For example, while you may live to 88, the last decade could bring impairments that make travel and mobility more difficult. Both average life expectancy and HALE are based on current health and mortality patterns, and are influenced by a number of variables, including geography, education and income. The figures above reflect the expectations for Canadians with an annual income in the fourth quintile — between $90,300 and $145,000.

Esme Fuller-Thomson, Professor and Director at the Institute for Life Course and Aging at the University of Toronto, points out that working life can also be stressful, and many people would prefer not to work into their 60s, let alone their 70s. Those gifted with extra years of health might consider retiring to enjoy those healthy years as best they can.

Fuller-Thomson, whose own mother worked until age 88, says one benefit of working is that it can stave off cognitive and physical decline, which can happen in retirement if people don’t stay active.

“But if going into work is something you dread, don’t do any more of it if you can possibly afford not to. I’m fearful some people keep working because they don’t know anything else — that’s not great. But if you are excited about going to work, well, then you’re in the right place,” she says.

"Delaying retirement could add 10 years of compound growth, presumably on a large portfolio — it's growth on growth on growth."

The idea of working an additional decade past traditional retirement age may be limited to those who are physically fit, who also enjoy their work and those who are in a fortunate financial position to make that choice for themselves. The age at which you retire may not be a conscious choice for all Canadians: Some may be forced into retirement by their employer. Others still might continue to work because they need the income.

Ewing says that whether you retire at 65 or not, another decade of healthy living could change many financial assumptions for Canadians at all ages. Here are some of the things you might consider.

If you had 10 extra years, you could…

Keep earning Ten more years of income could mean significantly higher savings, particularly if your mortgage is paid off and you’re no longer funding your kids’ education. Plus, delaying Canada Pension Plan/Quebec Pension Plan withdrawals until you are 70 could bring higher monthly payments. A wealth advisor could help determine what’s right for you.

Change careers A working span of 40 years instead of 30 could create time for more opportunities. For example, a career change in your 40s might be an awfully tough choice for some, but with an extra decade ahead, going back to school, completing an MBA or starting a business might look more practical.

Buy that vacation property If you are mid-career and think you’ll retire at 60, you might think hard about buying a cottage or chalet, Ewing says. Having another decade to pay it off could change the calculus. Besides enjoying the obvious benefits of owning a cottage, you could acquire a jewel of an asset to pass to the next generation.

Retire when you feel ready Spending more time at the office is not for everyone. If you can, why not spend your extra healthy years enjoying yourself? That could mean more time for travel, leisure activities or spending time with grandkids and the rest of the family. A wealth advisor could help you explore your options.

Both Ewing and Fuller-Thomson agree that people shouldn’t spend their remaining healthy years working simply for the money. But buoyant health as an older adult could open up more options, not just when you’re older, but earlier in life as well. Talking to a financial planner could help to focus your ideas and turn them into reality.

DON SUTTON

MONEYTALK

ILLUSTRATION

DANESH MOHIUDDIN

- Laura D. Quinby and Gal Wettstein, Are older workers capable of working longer?,Center for Retirement Research at Boston College July 2021, Number 21-12, © Laura D. Quinby and Gal Wettstein, accessed Sept. 12, 2023, https://crr.bc.edu/wp-content/uploads/2021/06/wp_2021-8.pdf ↩