Estate planning considerations for blended families

Stepfamilies are common, but planning for who gets what after you die is anything but routine. When families come together, each with their own possessions, ensuring your assets go where you want is key.

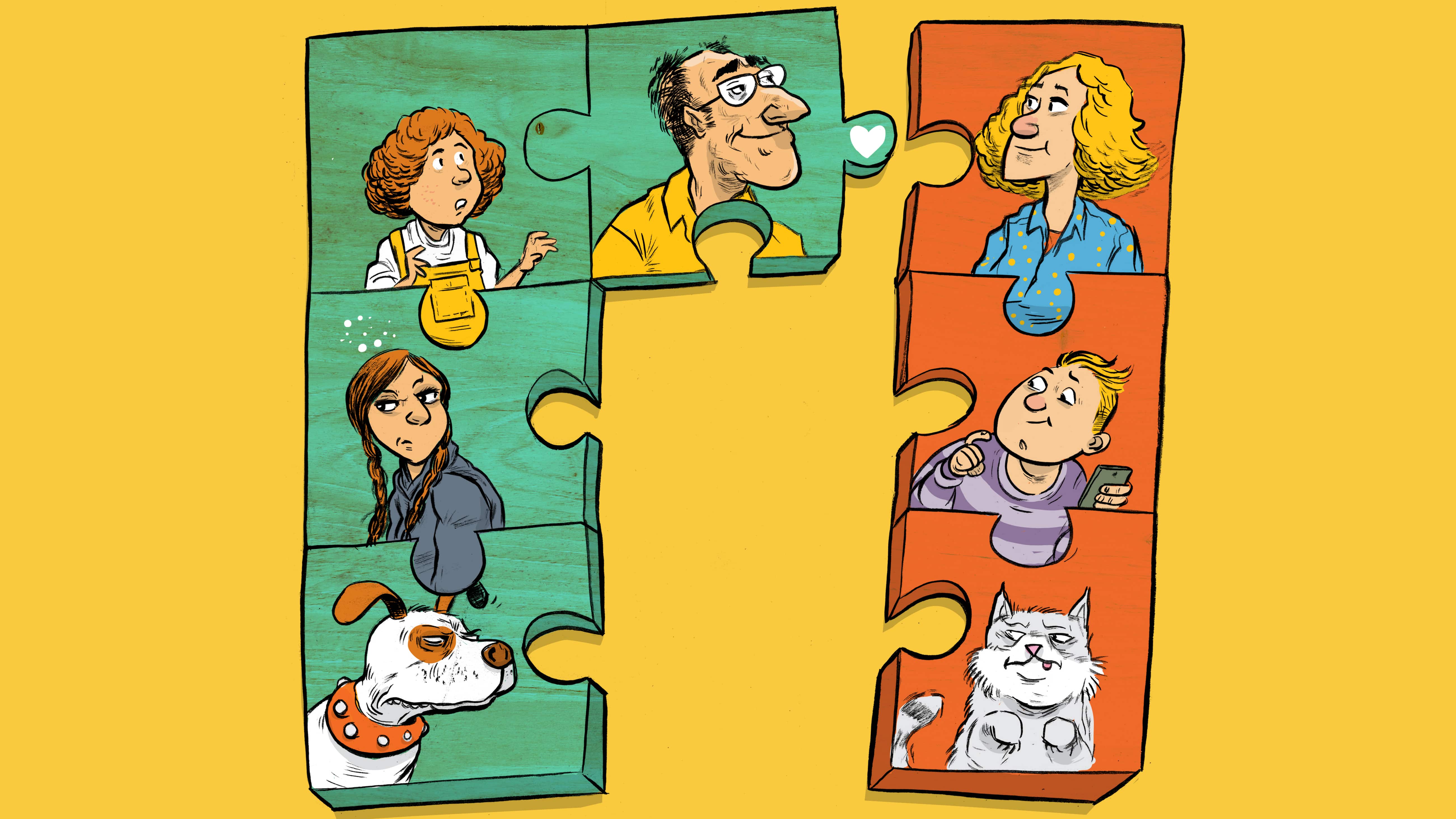

Marianna admits that her family life isn’t as idyllic as she’d like. She loves her new partner, but she has a strained relationship with her two grown stepdaughters. Her adult daughter doesn’t get along with them either. “The break-ups with our previous partners were not amicable,” she divulges. “The kids have not been supportive of our new family.”

It has made things difficult for Marianna and her new husband, particularly when it comes to figuring out how to build an estate plan. Marianna worries that if her husband dies first, a fight for his assets will ensue between herself and her stepdaughters. She also worries that if she dies first, her husband might inherit her property, remarry, and leave her daughter with nothing. “We’ve been planning for some time how to make sure everyone is cared for, even after one of us is gone,” she says. “And since we both came into the relationship with our own wealth, we want to pass our own assets on to our own children.”

The last Canadian census reported couples that come together with children from previous relationships represent one in 10 families.1 TV sitcom scriptwriters may write to show Dad would have left everything equally to Mom, all the stepchildren, and of course, their beloved housekeeper. In reality, blended families rarely work that way. It stands to reason that many people who remarry may want to protect the wealth they came into the relationship with, and although they want to ensure their significant other is taken care of when they’re gone, they want to pass down their wealth to their own children as well.

Nonetheless, it’s common for people in blended families to leave everything to their new partner. Although your intention may be for an inheritance to go to your kids after you and your partner are gone, there is nothing to stop your surviving partner from writing a new Will that leaves everything to their heirs, or spending it — effectively disinheriting your kids.

So how do you ensure your estate goes to your children while leaving enough for your spouse?

“It is exponentially more complicated,” says Tannis Dawson, a High Net Worth Planner with TD Wealth. “Each spouse will want to protect their children and their children’s inheritance while navigating what the law requires and what their moral and emotional obligations are to all parties. This may be harder to accomplish with blended families.”

“Each spouse will want to protect their children and their children’s inheritance while navigating what the law requires and what their moral and emotional obligations are to all parties.”

TD WEALTH

Harder to accomplish maybe, but not impossible. Here are some tools in your estate planning toolbox that can help you protect your own wealth and assets, while providing for loved ones as you intended.

A battle of Wills

Most people believe a well-worded last Will can execute their wishes perfectly once they are gone. Without a Will, your loved ones will likely find it difficult to manage your estate, as well as your wishes for your children and their care. Spouses often create reciprocal Wills, where the wishes of the husband and wife are exactly the same. So in essence, assets are left to the surviving spouse, and then, once they are both gone, any leftover assets are distributed to the children in equal proportions. Sounds fair, right? Well, consider the possibility that a surviving spouse remarries, and a new spouse squanders away the inherited assets, leaving the stepchildren with nothing. Even if the surviving spouse fulfills the wishes of the deceased spouse and includes the stepchildren as beneficiaries, assets that are spent and gone are gone, and can’t be passed on.

And even though a Will allows someone to distribute their assets any way they wish, the law may throw up other issues. Legally, spouses and biological or adopted children (not necessarily stepchildren) may have rights to an estate after death.2 Because of that, opposing members of blended families can end up fighting after someone passes away. “Biological children and stepparents can end up in a tug-of-war over assets,” says Dawson. “While a Will can be a very important part of estate planning, it may not be the be-all and end-all.”

A matter of trust

In addition to a well-worded Will or testament, the use of trusts can be an effective tool in estate planning — and may be a good strategy for blended families. A testamentary trust that is created in your Will takes effect upon your death. You can place assets in a trust, dictate their use, as well as ownership, and users and owners can be different. This may be an appropriate solution in the case of a family home where a surviving spouse lives, but ultimately will be owned by the stepchildren down the road.

Marianna would like the family home to be used by her husband until his death, after which the home would be sold and the proceeds split 50/50 between her child and her husband’s daughters. A trust may allow her to do just that. “Spousal trusts are often used to provide for a second spouse while, at the same time, ensuring that the money or assets will ultimately flow through to your children and descendants. This way, assets can only be used the way you intend and are protected from third-party claims, your new spouse’s own wishes or remarriage or poor planning,” says Dawson, adding that the tax consequences and timing of the future sale needs to be considered in the plan too as children will not be able to receive the proceeds until the spouse passes away.

Joint ventures

Joint accounts can be used as a form of estate planning, particularly by those who want to pass money or investments directly to their children. Marianna has an investment account with her daughter that will be owned by the last to die. With a joint account, it is a common misconception that the account won’t become part of the estate to be distributed and that it would be passed down directly instead.

The fact is that there are no guarantees that a joint account between a parent and adult child will escape becoming part of the estate. Case law suggests that when the joint account holders are a parent and adult child, there’s a presumption that the money in the account is there to deal with the management of an elderly parent’s finances unless there is a deed of gift that clearly shows the intent.

“Biological children and step-parents can end up in a tug-of-war over assets.”

TD WEALTH

After death, therefore, a probate court may view the proceeds as part of the parent’s estate and distribute it to those who have a claim to it. “For this reason, where the survivor of joint account holders believes they are entitled to the balance of the account upon the first death,” says Dawson, “it’s necessary to get legal advice to establish that intention of the right of survivorship from the get-go.”

Benefiting beneficiaries

Carefully listing beneficiaries on registered accounts and pensions is one way to direct assets to the people you intend. The beneficiary designation is powerful, but watch if the Will is dated after as it may trump that. For assets where a beneficiary is named, such as RRSPs and RRIFs, those assets will bypass your estate and go directly to the beneficiary. That’s why it’s so important to keep your beneficiaries up to date. “If an ex is listed as a beneficiary on a pension or a registered account,” Dawson says, “they could very well get a payout — even if you are now single or remarried.” Also be careful if one of the beneficiaries listed has passed away as you might disinherit that line as it will not pass to their kids as it might through the Will.

Give it away now

For many, in blended families or not, giving away assets before you die is becoming increasingly common. You can see the effect of your gift and specify use while you are still living. With proper financial planning, gifting can also minimize any taxes upon death, and even reduce your tax burden now. And for those in blended families, a gifted asset will go to exactly who you want it to go to.

Of course there are some downsides — namely the possibility that you may need those assets before you die, particularly if you live a long life or have significant care needs down the road. You also will have little control over the future use of the assets once gifted, so if you wish to gift money now for a child’s future education, there is no guarantee that the money will be used for that purpose after you are gone. You are also paying tax now compared to on your passing.

Marianna is confident that she and her new partner will provide for each other in their estates, but really hopes that whatever bitterness there is now between the children and stepparents dissipates. “I get the feeling that once we are gone and the estate is settled, the children will go their own way,” she says with a sadness. “We forced them to be family. When we’re gone, those family ties will be too. But at least everyone will have what they’re entitled to.”

— Denise O’Connell, MoneyTalk Life

- Statistics Canada. 2016 Census Families and Households Highlight Tables. Ottawa, Ontario. 2016↩

![16-03-22 Asked To Be An Executor Read This First- TD MoneyTalk Life Story Illustration [Feat]](https://www.moneytalkgo.com/wp-content/uploads/2016/03/Asked-To-Be-An-Executor-Read-This-First-TD-MoneyTalk-Life-Stories-Feat-1.jpg)