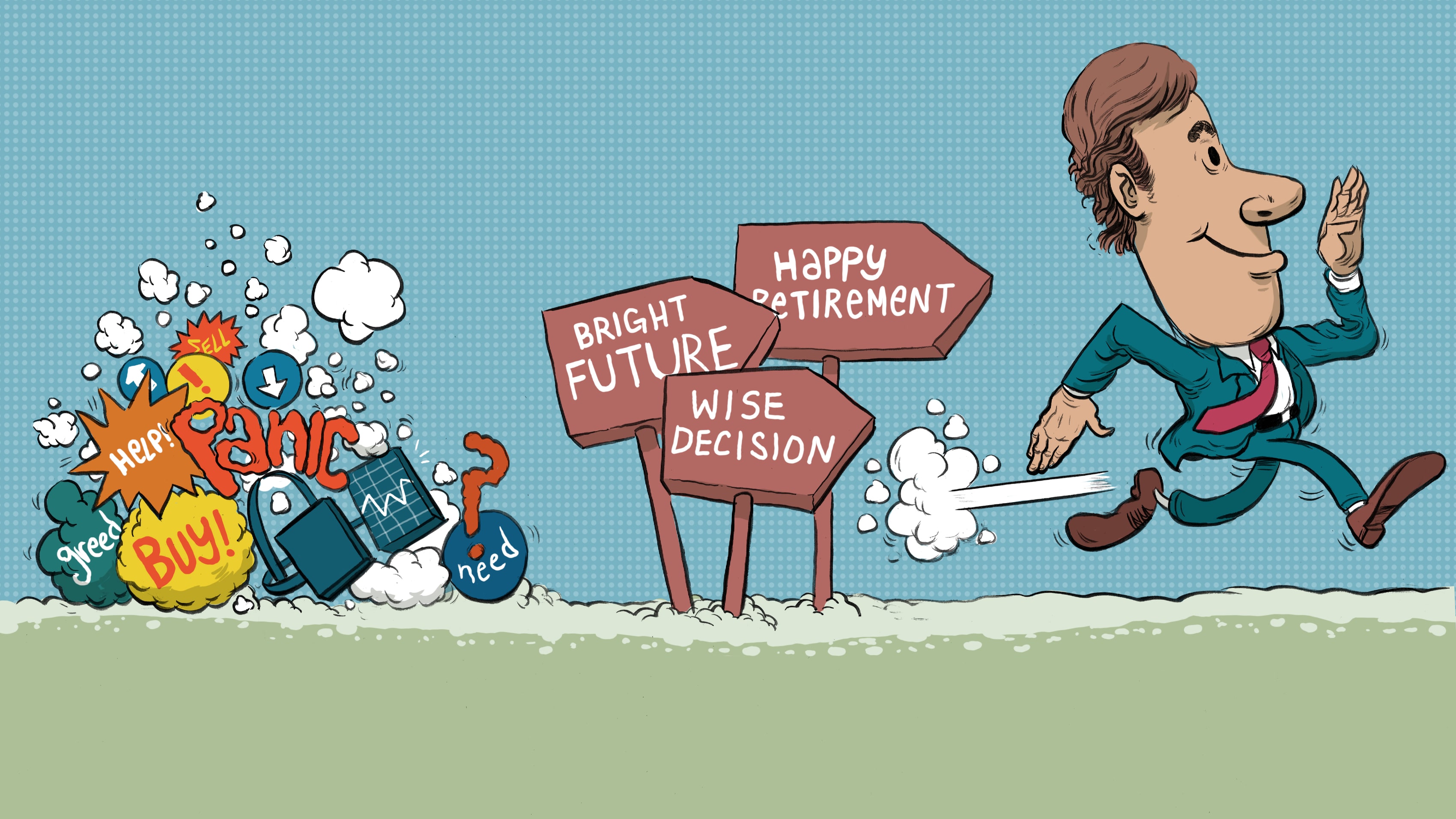

Discover Your Investing Blind Spots

Behavioural Finance: People can learn to be smarter with money when they understand how their actions may be sabotaging their investing decisions.

Originally published April 2017

Your favorite tech stock has not been co-operating. It gained significantly when you bought it but now it has declined into the loss area. You love the product and are an enthusiastic customer so you are still confident, and you buy more shares. But it drops in price considerably. Still, you remember how quickly it rose into positive territory, and you buy more shares. Yet it declines slowly, then abruptly loses a quarter of its value. Disappointed but still attached to your favorite stock, you feel that that the time for it to regain its potential is just around the corner and so you bide your time…

The above scenario is common among investors and is a prime example of how human behaviour can conflict with investing behaviour and pull reasonable people into ill-advised actions. In this case, it’s having a favorite stock and then chasing its price downward instead of cutting your losses.

And yet common investing mistakes — impulse buying, putting off important decisions, blaming others for your bad decisions — are repeatedly made by investors. Understanding why this happens and how to avoid these behaviours can be best explained through behavioural finance.

Behavioural finance is the study of how people make decisions in relation to money. It’s a social science concerned with how our emotions, patterns of behaviour and “blind spots” dictate our decision making. Sometimes we are able to make rational financial decisions after assessing all available facts and information. At other times, our decisions may not be so rational, and are driven by our emotions, which may not lead to the best outcome.

In our scenario above, the behaviour — a resistance to cut your losses — is detrimental to long-term investing goals. It is reasonable to become attached to a pet or a piece of music but a stock shouldn’t be the object of any affection. By realizing we have decisional blind spots that lead to less than optimal outcomes, we may either take action to avoid financial mishaps or engage the help of others to keep us in check. Either way, the goal is the same: to make better financial decisions.

Dilip Soman, Professor of Marketing and the Corus Chair in Communications Strategy at the Rotman School of Management, University of Toronto, says that the study of behavioural finance is the ‘marriage between psychology and finance.’ In contrast to other aspects of finance and economics, which assume an ideal model where people always make ‘correct’ decisions, behavioural finance analyzes how people actually make financial decisions, not how we think people should make those decisions.

Soman says to understand our behaviour towards investing is to remember that the human brain evolved to focus on the fundamentals of survival, food, shelter and procreation. While humans obviously have the ability to think beyond those essentials, create civilization and deal with complicated economic and financial concepts, the complex nature of the decisions we need to make results in decision biases that can continue to trip us up.

Just as we can convince ourselves it’s ok to eat ice cream when we are trying to lose weight, so too we can make wrong turns when making financial decisions. If we are conditioned to learn or interpret information a certain way, we can misapply the pattern of thought or data. As well, the human brain is quite successful at fooling itself into believing future scenarios based more on rose-coloured glasses than reality, he says.

But Soman thinks people shouldn’t get demotivated when they hear they probably make poor decisions around money. It happens to many people despite our best intentions, high intelligence or long experience in the area.

“I think we have developed the financial markets, as indeed, many other business markets, so that they essentially stretch the human mind more than it has ever been stretched. The fact people get it wrong is not a surprise and should not be considered a failure. The fact that often times we think people should get it right is just more irrational behaviour,” he says.

Soman says there are recurring biases that occur that everyone should be aware of. Realizing that you are prone to these actions may help you avoid them and become a more aware investor. Awareness could lead to better decision-making, and ultimately a better return on your investment.

Common Financial Blind Spots

Resistance to taking losses and profits: If I had cash, would I buy this investment at this point?

Description: When we continue to invest money, time and effort into a failing stock or investment plan because we have put so much energy and emotion into it.

Example: As we saw in our opening illustration, resistance is refusing to sell a losing stock in the hope that it will recover or even (Yikes!) doubling down on a losing stock as our over-confidence outruns our rationality. On the opposite end of the spectrum, an investor might refuse to lock in profits when a stock rises significantly, thinking the stock will always continue gaining more value. At some point, all stocks retrace their steps and the party is over.

Soman says resistance is also known as the escalation bias or the “Concorde fallacy;” Britain and France had so much economic and political capital invested into building Concorde supersonic aircraft in the 1970s that they continued manufacturing long after it was financially rational to do so, to the detriment of their governments and budgets. In investing, people mistakenly put emotion into their decisions and, like leaving a partner, breaking up with a beloved company is often hard to do. As an investor, you may consider this: ‘If I had the cash, would I buy this declining stock at this point? Would I buy this soaring stock at his point?’ The answer will help you decide what you should do in your current situation.

Strategy: Soman says often people don’t give up on their bad investment plans or sell their losing stocks (or stop funding aircraft) because to do so is to admit failure, and admitting failure to some people is too high a price to pay, worse than saving money or investments. Best to chalk your error to a learning experience. Satisfy your bottom line, not your ego.

All plan but no action

Description: Making a plan but not executing it.

Example: Setting up an RESP when a child is born to fund education but not contributing and receiving grants. Result? There isn’t enough money to fund university when the child grows up.

Everyone has experienced making plans and not fulfilling them. Soman likens our behaviour to a planner-doer dichotomy which resides in us all. The planner makes the plans, but unfortunately, the doer is faced with the reality of carrying out the plans and that’s when plans go astray. A planner will set an alarm for 6 am intending to get up early and get many things done. The doer hears the alarm and — after a late party — hits the snooze button and nothing gets done.

Soman says the invention of an alarm clock that runs away before you can hit the snooze button allows technology to help the planner get the doer literally up and at ‘em.

Strategy: For many of us, the financial equivalent of a run-away alarm clock is defined automatic investments and savings plans, where contributions come directly off our pay cheque or savings account. This allows us to make a plan once, and set up a mechanism that will automatically fulfill our goals without more effort from our part.

Framing

Description: When we respond differently to the same outcomes.

Example: Losing $400 on the street and on the stock market will provoke two different internal reactions. You probably feel angry and foolish at losing money on the sidewalk, and disappointed losing $400 in the market.

We rationalize that when investing, we have to assume a certain amount of risk and, over time, we will have gains and losses. We are philosophical about short-term losses because we know the long-term result is what counts, or at least we hope we can make up the loss with our next winning stock. However, we are less forgiving that sometimes people are forgetful or distracted (as humans are) and will lose things – like cash.

Consider this situation. If an investor is told that they have lost 2 per cent of the value of their $1.5 million portfolio during a sudden market disruption, they may feel unhappy but not panicky. If they check in with their portfolio and realize they have lost $29,675 in one day, they may panic and sell off their entire portfolio in a hysterical rush to avoid more losses. In this case, when the loss is framed in percentage terms, it causes a mild reaction but when the loss is framed in hard dollars, it provokes an overreaction.

Strategy: Soman says reframing a problem in different ways allows us to change the context of the problem for better or worse, usually allowing us to snap on rose-coloured glasses to minimize problems. In investing (and in a more realistic example) this could be celebrating a 5 per cent one-day gain for a stock that makes up 1 per cent of our portfolio but ignoring economic aspects like interest rates or foreign exchange fluctuations that actually mitigate overall gains. Being aware that we do this may bring some rationality to our decisions and make us smarter investors.

Short-Term Focus

Description: Putting undue emphasis on events that are closer in time and minimizing events that are further away.

Example: Many Canadians are not saving enough for retirement.1 At the same time, the ratio of household debt to income continues to rise. This suggests that people are choosing to spend now and forego saving for the future.2

THE $110 OPTION EXPERIMENT

Option 1

Would you choose $100 now or $110 in a week?

A certain number of Dilip Soman’s students (irrationally) choose the immediate $100 despite the potential 10 per cent gain by waiting seven days.

Option 2

Would you choose, $100 in 52 weeks or $110 in 53 weeks?

With this choice, the students overwhelmingly pick the $110, because both values are so far in the future there is no discernible advantage to getting one sooner. Yet, a seven-day wait is the same difference between both situations.

Strategy: Again we can trace this problem back to our ancestors, Soman says, who naturally evolved to focus on immediate emergencies. In our modern age, the day’s priorities continue to fight for our attention. Thinking about retirement 30-years away takes a back seat to working for a living, caring for children, running a household, sitting in traffic and the other myriad demands on our time.

Soman says the $100 option experiment (above) shows the problem we all face, that we categorize time. Anything in the present has a higher importance than anything in the future which has lesser significance. This, coupled with a problem of motivation toward far-future events, often leaves us shuffling our feet when it comes to making decisions about important — but far-off — events like retirement savings.

Many Canadians are putting off retirement plans and are overspending but a short-term focus creeps into their investing plans as well. Putting together an investment plan is great but if the plan isn’t evaluated at least annually, it can quickly go awry. Yet many people have investments plans that are out-of-date but put off fixing their investments because too many of life’s distractions get in the way. Having an eye on the long term and not letting short-term problems distract should be the mantra for all investors in order to fulfill long-term goals like an affluent retirement.

Over-Confidence bias

Description: Attributing success to yourself but failure to other influences.

Example: Being proud of yourself that your stock pick did well, but blaming your financial professional, the stock market, the economy and the universe if your investment moves perform negatively.

Soman thinks that the self-attribution bias has to do with how much control we have over our particular environment — or how much control we think we have. If we do our homework and complete due diligence before we make a stock trade, we are apt to attribute success or failure to ourselves. However, if we enter into a situation where we have less control, such as our children’s education, the situation is different. We are apt to attribute a kid’s success at school to the child but their lack of success on their teachers, the school or the education system. Similarly, if you are unaware of external events, and your portfolio is down this month, you’re more apt to blame your financial advisor than yourself or market cycles.

The problem with attaching success to yourself or failure to a financial advisor without cause is that you may mistakenly grant yourself wisdom and experience you don’t actually have. Because you made a successful securities trade, you could become overconfident in your skills. If the markets have a poor week, you may lose confidence in your financial planner for no good reason. This rationale can get you into trouble and lead to bad decisions. If you begin thinking you are a financial genius when you are playing with your retirement savings, it may not end well.

Strategy: Irrational overconfidence in yourself or lack of trust in a financial advisor may jeopardize your investments and financial plan. In both cases, it may lead to poor decision-making based on emotions, not facts. Working with an investment professional who understands your financial biases may help illuminate those investing blind spots.

Keep in Mind

Soman says that the more people learn about their behaviour in regard to money, investing and financial planning, the better prepared they will be when confronted with decisions, strategy and setbacks. However, mere awareness and even understanding your investing blind spots may not be enough to correct your behaviour. We all know that to lose weight, we should eat less and exercise more. But not many can carry out that seemingly simple proposition successfully because of our ingrained behavioural patterns. Many turn to self-help books, nutritionists, doctors and life coaches for help. Similarly, to overcome your financial blind spots, you may need to consult financial professionals who understand your particular biases, and together, design a plan that fits your lifestyle and goals.

— Don Sutton, MoneyTalk Life

- Is reality biting Gen-X when it comes to retirement savings? TD survey finds one in three Gen-Xers expect to work post-retirement, TD Bank, Nov. 26, 2016, accessed Mar. 2, 2017, http://td.mediaroom.com/201611-24-Is-reality-biting-Gen-X-when-it-comes-to-retirement-savings-TD-survey-finds-one-in-three-Gen-Xersexpect-to-work-post-retirement ↩

- Rachelle Younglai, Canadians keep digging themselves deeper into debt, The Globe and Mail, Dec. 14, 2017, accessed Mar. 02, 2017, theglobeandmail.com/report-on-business/economy/canadas-household-debt-risesin-third-quarter/article33318488/ ↩