After a year of choppy markets, rising inflation and the threat of a recession, you might feel like you need to give your entire investing approach an overhaul. However, smaller tweaks to your portfolio can be just as important to your financial goals. Even if you are worried about a potential pullback in 2023, there are a few moves to consider for your portfolio that may help to grow your savings in the year ahead. Here’s how.

Look for free money

As you welcome in 2023, take a moment to make sure you’re not passing up any free money in the form of government grants or employer benefits. Here are a few of the programs to capitalize on:

- Pension plans If your employer offers a pension plan, it can be in your best interest to join. Employers will often match your contributions up to a certain level, giving you an instant return on your investment.

- Group RRSPs Similar to a pension, some employers may match your contributions to a group RRSP.

- Employee-share ownership plans Some companies offer employees shares in the business as part of your compensation or allow you to buy shares at a discounted rate.

- Canada Education Savings Grant When you contribute to an RESP, the government will match up to 20% of your first $2,500 in annual contributions to a maximum of $500 a year or a lifetime limit of $7,200. This grant can make even small amounts worthwhile.

Get ahead of the curve by taking full advantage of your TFSA

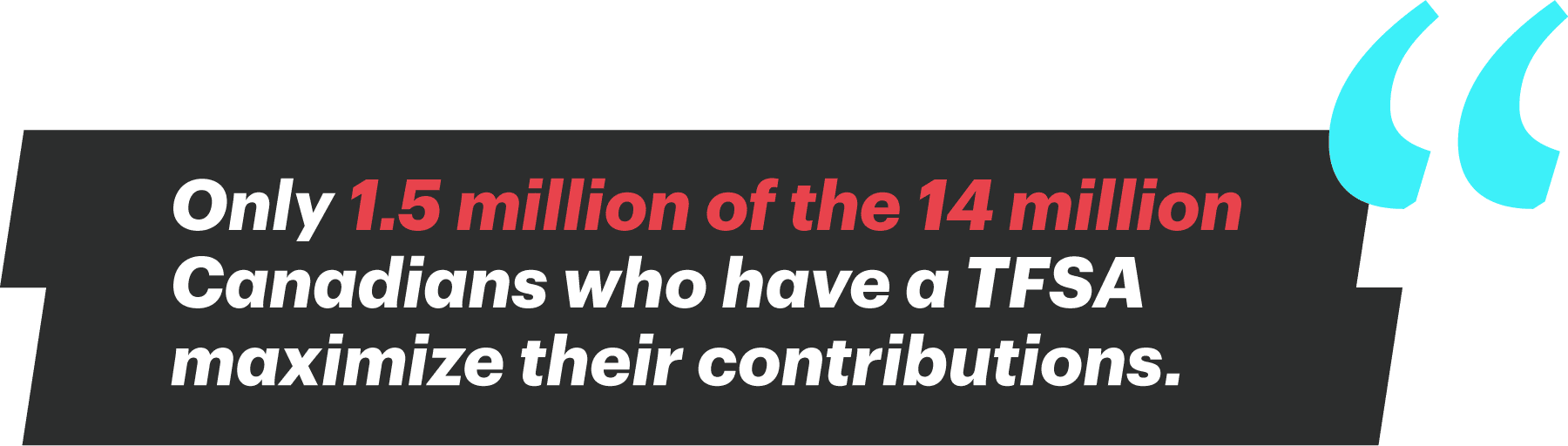

A Tax-Free Savings Account (TFSA) is one of several different account types that can help you grow your money. Still, only a small percentage of Canadians take full advantage of these accounts. The latest data from the Canada Revenue Agency suggests only 1.5 million of the 14 million Canadians who have a TFSA maximize their contributions.

With the annual contribution allowance rising to $6,500, up from $6,000 in 2022, you would need to contribute roughly $540 a month to max out this year’s contribution limit. Don’t give up if you don’t have that in your budget right now, even half that amount can help you get ahead. That’s about the same as what you would spend buying your lunch at the food court during the month. Here are a few important things to remember about TFSAs:

- In a TFSA, any interest, dividends or capital gains you earn on your contributions grow tax-free, allowing your investments to compound faster. These accounts can hold a variety of investment vehicles such as GICs, stocks, bonds and exchange-traded funds (ETFs).

- One way to build your savings with the lowest effort possible is to set up automated contributions so that they coincide with your payment period, or another frequency that works for you. Once you’ve automated the process, you’ll miss that money less than if you have to manually transfer it online. Start with an amount you know you can afford and try to raise it over time.

- If you’re already making regular contributions to your TFSA, the start of the year is the ideal time to make sure you’re aware of how much contribution room you have available. The contribution room for 2023 is $6,500. If you were 18 or older in 2009, the year the TFSA was introduced, and have never contributed, you’d be able to contribute $88,000 to your TFSA in 2023.

- Finally, if you removed money from a TFSA last year, you can recontribute that amount starting this year.

Rev up your RRSP

RRSPs are the number one retirement savings option in Canada. In 2020, 6.2 million Canadians invested $50.1 billion in their RRSPs. As the year changes, it may be a good time to check in on your account to make sure you’re still working toward your retirement goals.

- RRSP season is generally thought of as the period leading up to the RRSP contribution deadline, which, for the 2022 tax year, is March 1, 2023.

- Better yet, consider making a lump sum contribution earlier or automating RRSP contributions by investing the same amount every month. Not only is this a great habit, you’re also paying yourself first at regular intervals without lifting a finger. This method will help you avoid the deadline crunch at the end of the year.

- There may be other ways to free up some of your take-home pay if you are contributing to your RRSP or a group RRSP through payroll deductions. You may be able to reduce how much income tax gets deducted from your paycheque by filling out a T1213 Request to Reduce Tax Deductions at Source form, which could help offset the money you’re putting towards your retirement.

- Commit to leaving your RRSP intact. If you see your RRSP as a source of emergency funds, think again. A TFSA may be a better spot to keep that sort of money because, unlike an RRSP, you can withdraw funds tax- and penalty-free.

- If you have many different RRSP accounts, consider consolidating them into one account to potentially help you save on fees. It will also make it easier for you to manage your RRSP and may help you to capitalize on more money-saving opportunities.

Review RESPs

If you have children and haven’t yet set up RESPs for them, making that a priority for 2023 can pay off in the long run. RESPs are tax-sheltered investment vehicles intended to help fund a child’s post-secondary education. And they’re a great way to save, especially as the price of college and university tuition continues to rise. Just remember that with RESPs, there is a $50,000 lifetime maximum that you can contribute per child.

- Like TFSA and RRSPs, automating your RESP contributions will help ensure you don’t skip annual contributions — and the government grants that come along with them.

- Grandparents and other family members often want to give meaningful birthday and holiday gifts, and RESPs can be a great way for them to help fund your child’s education. Consider asking other family members donate to your child’s RESP.

Don’t ignore your investments

It’s been a volatile year in the capital markets with large swings both up and down. It’s a good idea to take stock of how things have gone and and whether or not you should re-evaluate your portfolio decisions as 2023 begins.

- Make sure your asset mix is still aligned with your goals. This may mean diversifying more broadly.

- Consider learning about asset classes you haven’t in the past. Every sector responds differently to market conditions. For a better understanding of asset mix, check out TD’s Investor Resource Centre.

- Review your risk profile (conservative, moderate or aggressive) to determine if it still reflects your investing temperament. Analyze your financial needs, reset your investment preferences and rebalance your portfolio if necessary.

Taking small, constructive steps, even in a time of economic uncertainty can help contribute to your overall goals. If you haven’t in the past, this year, make a resolution to invest in yourself by making small changes to the way you manage your money. Unlike resolutions like hitting the gym or going on a diet, if you optimize your portfolio and automate your savings, you may not need to change any day-to-day habits to make a difference.