A Winning Personality:

How It Contributes to Financial Success

Originally published October 2017

Contrary to what people believe, financially successful people often don’t have special know-how or skills when it comes to investing and saving. In fact, studies show that reaching financial goals has to do more with having a specific set of character traits. MoneyTalk Life spoke with Dilip Soman, behavioural economist and professor of marketing at the University of Toronto, about the specific personality types that may have a better chance at succeeding financially relative to others. The good news? Even if we don’t have those personality traits, we can work on developing them, and that might lead to financial success down the road.

Dilip Soman

Behavioural Economist, Professor of Marketing, Rotman School of Management, University of Toronto

Dilip Soman holds the Corus Chair in Communications Strategy. His research is in the area of behavioural economics and its applications to consumer wellbeing, marketing and policy. Prof. Soman served as an associate editor of the Journal of Marketing Research, and on the editorial boards of the Journal of Consumer Research, Journal of Marketing, Journal of Consumer Psychology and Marketing Letters. He was recently named as one of the “professors to watch for” by the Financial Times (London) newspaper. He is the recipient of several teaching and research awards.

Q. Is managing money more about skill and know how, or is it about a specific set of character traits?

A. There are indeed skills and knowledge sets necessary, but there are a large number of psychological principles at play in managing money. Many of these principles are trait-related (good habits and practices) and many others are context dependent, like how we make decisions, and how we handle emotions in certain situations. That said, character traits like patience, thoughtfulness, empathy and long-term orientation play a very large role in creating success in money management.

Q. How do these personality traits affect investing?

A. Patience for example, will allow investors to take the time needed to weigh all the information available to them, and make prudent decisions. Also, people who are “planners,” whether on paper or even just in their mind, tend to be forward-looking and take action accordingly which makes their goals tangible. Conversely, impulsiveness may sabotage your finances because you react rather than reflect when you have decisions to make. Being a “follower” may make you susceptible to all the noise out there when it comes to what you should do with your money.

Q. Do studies and research show that personality plays a big role in financial success?

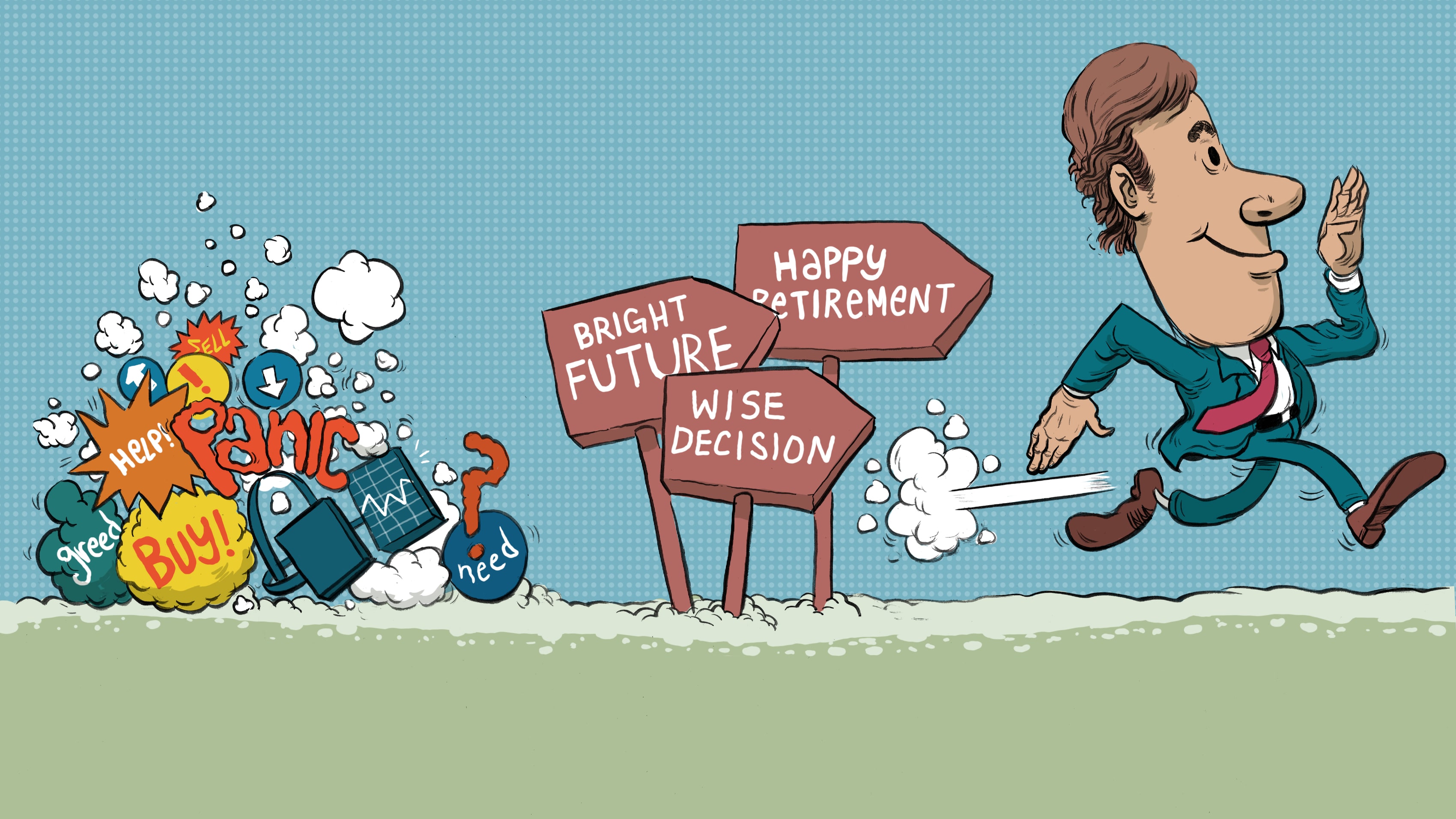

A. I am not aware of many large-scale studies that look at the effect personality has on financial success directly. However, many individual difference variables — traits that you can see as components of personality — do play a role in financial success. We know, for example, that overconfidence and impulsiveness are detrimental to long-term success, as is myopia and the need to check portfolio balances regularly.

Q. How can personality help achieve financial success?

A. By breaking down personality into it constituent behaviours and understanding the role that each plays in financial success, we can start identifying the specific personalities that can help financial decision-making and better train people to spot behaviours that are working against financial success.

Q. How can you foster those personality traits?

A. It’s really a two-stage process. The first stage is awareness — simply making people aware of their personality and decision-making blind spots can get them to slow down and contemplate the consequences of their decision. They might have a tendency to panic when the markets are down, or might assume that if their investments are “winning”, that the streak will continue. The second stage is training. Training is not merely education, but also a lot of practice and feedback. For instance, we could develop planning prompts, tip sheets and decision-making tools and encourage people to use them routinely. By comparing outcomes from decisions made without these tools to decisions that use these tools, the consumer is likely going to be able to see the effects of these traits and behaviours on their financial decisions and well-being directly!

There are many considerations when deciding where to put your money, and everyone’s priorities and situations are different. So talk with a financial professional who can help you weigh your options. You’ll need to consider your financial goals, whether they are short-term or long-term market conditions, and your tolerance for debt and risk. And ideally, your final decision may come down to which goals or priorities are more important to you.

— Denise O’Connell, MoneyTalk Life